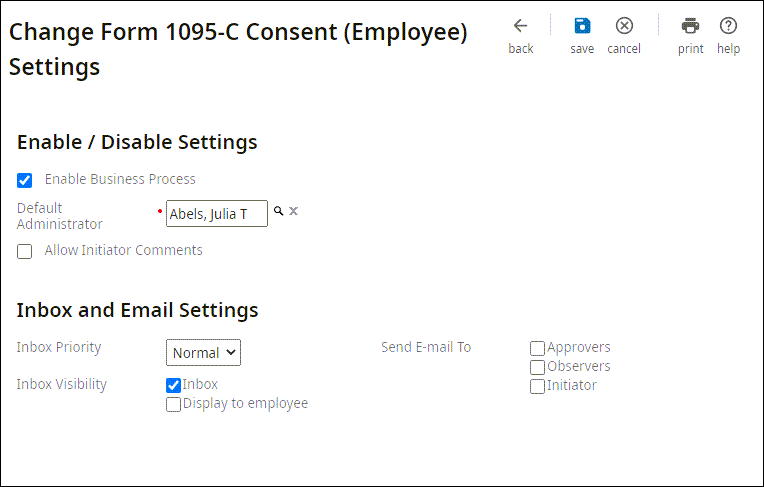

Configure the 1095-C Consent Form

Configure Employee Forms 1095-C Electronic Consent

In accordance with federal laws regarding Forms 1095-C, employers must provide a Form 1095-C to each of their full-time employees on paper, unless employees provide consent electronically to receive the paperless version of the form.

Individual employees can designate whether they want Form 1095-C in a paper or electronic format using the Change Form 1095-C Consent page. To consent to receive the form electronically, system administrators must enable the business process and provide employees with Web access to the Form 1095-C page. The business process and Web access rights are delivered OFF by default.

- Select Edit for the Settings option to enable and configure preferences and

notifications for the business process.

Change Form 1095-C Consent

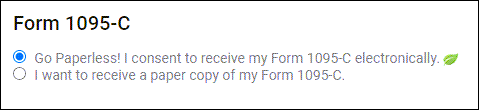

Employees can elect to receive a paperless copy of Form 1095-C by selecting the option on the Change Form 1095-C Consent page.

Individual employees are required to make this election themselves. After providing their consent, employees access the form when it is available using a Web browser to view and print the form. No need to wait for the mail to arrive or their manager to deliver the form. As long as employees provide their consent, access to an electronic form via a Web browser is legal. For more information, refer to the Furnishing Forms 1095-C to Employees section of the IRS instructions for Forms 1094-C and 1095-C.

- From the Form 1095-C Consent page, select the option to receive the form electronically.

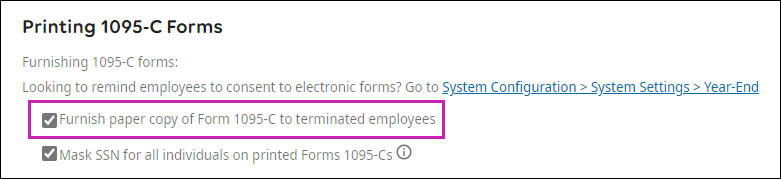

Configure Form 1095-C to Print for Terminated Employees

For terminated employees, use the terminated employee role, which provides former employees access to their Form 1095-C statements.

Administrators can also select the option on the Patient Protection and Affordable Care Act (PPACA) Reporting Settings page to print Forms 1095-C for terminated employees, regardless of whether employees opted for the paperless option.

- Select the Furnish paper copy of Form 1095-C to terminated employees box.

© 2022 UKG Inc. All rights reserved.

For a full list of UKG trademarks, visit www.ukg.com/trademarks. All other trademarks, if any, are the property of their respective owners. No part of this document or its content may be reproduced in any form or by any means or stored in a database or retrieval system without the prior written authorization of UKG Inc. (“UKG”). Information in this document is subject to change without notice. The document and its content are confidential information of UKG and may not be disseminated to any third party. Nothing herein constitutes legal advice, tax advice, or any other advice. All legal or tax questions or concerns should be directed to your legal counsel or tax consultant.

Liability/Disclaimer

UKG makes no representation or warranties with respect to the accuracy or completeness of the document or its content and specifically disclaims any responsibility or representation for other vendors’ software. The terms and conditions of your agreement with us regarding the software or services provided by us, which is the subject of the documentation contained herein, govern this document or content. All company, organization, person, and event references are fictional. Any resemblance to actual companies, organizations, persons, and events is entirely coincidental.

Links to Other Materials: The linked sites and embedded links are not under the control of UKG. We reserve the right to terminate any link or linking program at any time. UKG does not endorse companies or products to which it links. If you decide to access any of the third-party sites linked to the site, you do so entirely at your own risk.